Every Fraud Needs Three Things. Agents Just Made All Three Cheaper.

The anatomy of financial crime has not changed since the first wire fraud. What has changed is the cost of assembling the components. AI agents did not invent fraud. They industrialized it.

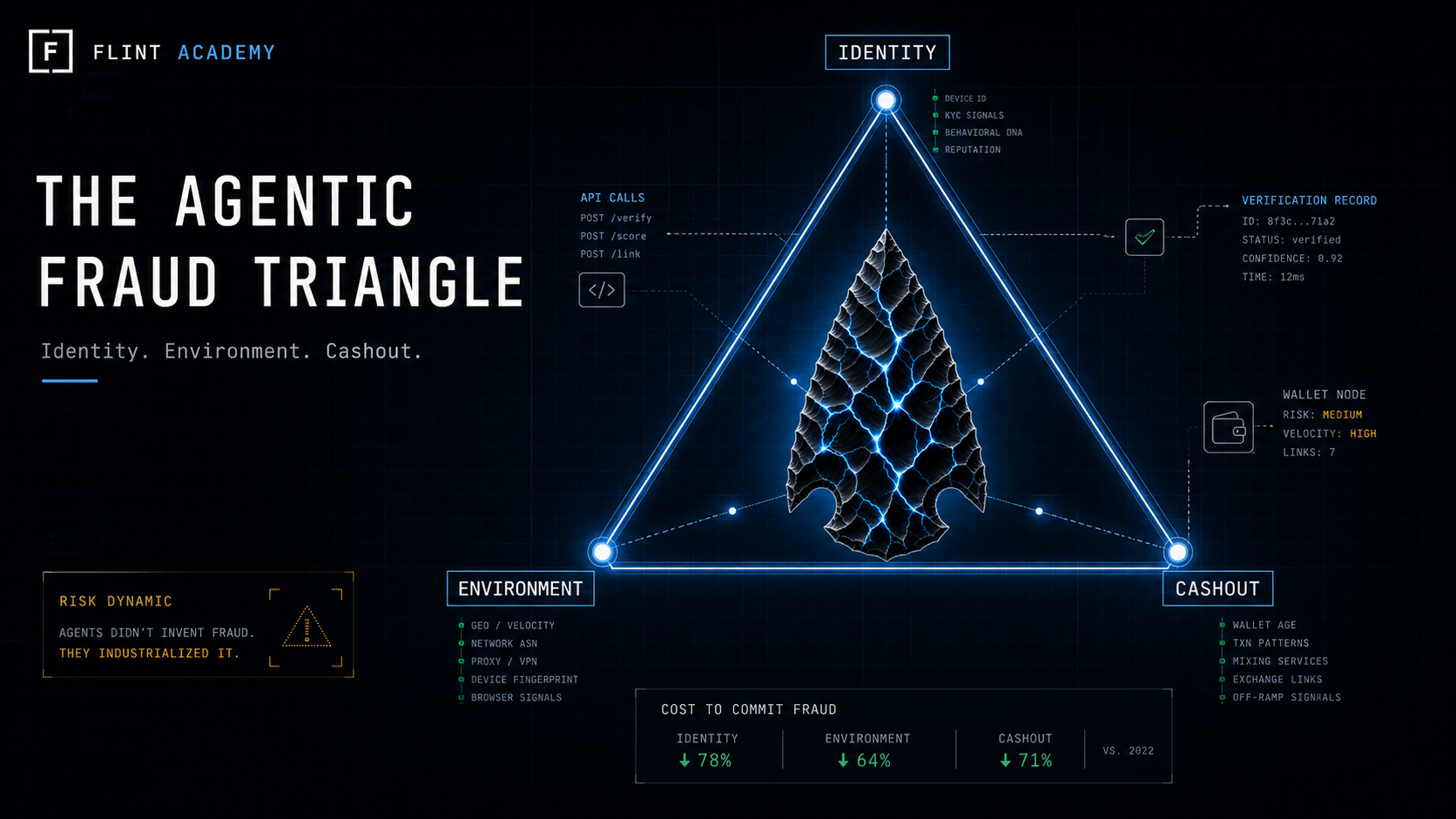

Every fraud investigation, no matter how complex, eventually reduces to the same three questions. How did the perpetrator establish a credible identity? What device or mechanism did they use to execute the transaction? And how did they convert the proceeds into something they could actually spend?

Identity. Device. Cashout.

These are not theoretical categories. They are the operational checklist that financial crime investigators work through on every case, from a $400 account takeover to a $400 million wire fraud. The specifics change. The structure does not. You cannot commit financial fraud without all three. Attack any one of them and the scheme collapses.

For decades, the fraud prevention industry organized itself around this reality. Identity verification systems made it harder to open fraudulent accounts. Device fingerprinting made it harder to operate from anonymous infrastructure. AML and transaction monitoring made it harder to move money without triggering a review. None of these defenses were perfect, but together they raised the cost of fraud high enough to keep most of it at a manageable scale.

AI agents just cut the cost of all three at the same time.

The First Leg: Identity

The identity problem in fraud has always been about plausibility, not perfection. A fraudster does not need a flawless identity. They need one that passes the checks in front of them.

For most of the last twenty years, that meant synthetic identity fraud: combining real and fabricated PII to create a profile that looks legitimate to a credit bureau or a KYC vendor. It is painstaking work. Building a synthetic identity with enough history to pass a bank's onboarding requires months of credit seasoning, careful management of the fabricated profile, and a working knowledge of exactly which data points each institution checks.

Large language models changed the economics of that process overnight. Generating a coherent, internally consistent synthetic identity, complete with a plausible employment history, a realistic digital footprint, and documentation that passes visual inspection, is now a task that takes minutes and costs fractions of a cent. The bottleneck that once required a skilled operator working a long con now requires a prompt.

For agents specifically, the identity problem is even more fundamental. An AI agent does not have a Social Security number. It does not have a credit file. It does not have an address that a data broker can verify. The entire identity verification infrastructure that the financial system built over the last fifty years assumes a human on the other end. When the entity is not human, the system does not return a bad score. It returns silence.

That silence is not neutral. It is an authorization gap. An agent presenting no identity signal to a legacy verification system does not get flagged as suspicious. It gets waved through because the system has no framework for what it is looking at.

The Second Leg: Device

Device intelligence became a cornerstone of fraud prevention because physical devices leave traces. A browser fingerprint. A hardware identifier. A behavioral pattern tied to how a specific person types, moves a mouse, or holds a phone. These signals are not perfect, but they are persistent. A fraudster who compromises an account still has to operate from somewhere, and that somewhere leaves evidence.

The device leg of the fraud triangle was never about catching bad hardware. It was about catching anomalous behavior tied to a specific execution environment. The question was always: does this device profile match the expected behavior of the account holder?

An AI agent is a device. It is also an execution environment, a behavioral profile, and an identity claim all at once. And unlike a human operating from a compromised laptop, an agent can be instantiated fresh for every transaction, run in an ephemeral container with no persistent fingerprint, route through a residential proxy network to mimic legitimate traffic, and terminate cleanly after the transaction completes.

The device signal that fraud teams rely on assumes continuity. The same person tends to use the same device, in the same location, at roughly the same times. Agents have no such continuity unless someone builds it in. A new agent instance looks identical to a legitimate first-time user. There is no behavioral baseline to compare against. There is no device history to check.

This is not a hypothetical attack vector. It is the default operating mode of any agent that was not specifically designed with persistent identity in mind. Most of them were not.

The Third Leg: Cashout

Cashout is where most fraud operations eventually fail. Moving money is easy. Converting it into something spendable without leaving a trail that leads back to you is hard. The history of financial crime enforcement is largely the history of attacking the cashout layer. Seize the accounts. Block the wires. Flag the structuring patterns. Make it expensive enough to convert the proceeds that the economics of the scheme stop working.

Stablecoins did not eliminate the cashout problem. But they changed its shape in ways that legacy AML frameworks were not built to handle.

A stablecoin transaction settles in seconds, not days. It crosses borders without correspondent banking chains. It can be split into millions of sub-cent payments that individually fall below every monitoring threshold ever written. It can be routed through decentralized exchanges, bridged across chains, and converted into other assets without touching a regulated institution at any point in the chain.

None of this is unique to fraud. These are also the properties that make stablecoins genuinely useful for legitimate commerce. The problem is that the controls that exist for traditional cashout, the CTR thresholds, the SAR triggers, the wire screening systems, were calibrated for human-paced transactions on regulated rails. They were not calibrated for an agent that can execute a hundred thousand transactions per hour across dozens of merchants without any single transaction crossing a reportable threshold.

The cashout leg did not disappear. It got faster, cheaper, and harder to see.

Why the Old Models Cannot Keep Up

The legacy fraud prevention stack was built on a reasonable assumption: the entity on the other side of the transaction is a human, and humans are slow. They make mistakes. They have habits. They leave traces. The controls were calibrated for human-paced fraud because that was the only kind that existed at scale.

That assumption is no longer safe.

A well-constructed agent-based fraud operation can cycle through synthetic identities faster than a KYC vendor can flag them. It can operate from ephemeral environments that leave no persistent device signal. It can move value across stablecoin rails in patterns that individually look like normal commerce and collectively represent a significant illicit transfer. And it can do all of this at a scale and speed that makes human review operationally impossible.

The response from the legacy vendors has been to add more data. More PII checks. More device attributes. More behavioral signals. The problem is that adding more data to a model that was designed to evaluate humans does not make it better at evaluating agents. It makes it more confident in wrong answers.

What the industry needs is not a better version of the old model. It needs a model that was built from the start to answer the question: is this agent authorized, by a known principal, to initiate this transaction, from this environment, at this time, for this amount?

The Verification Record as a Control

The fraud triangle is useful as a diagnostic framework. It tells you where to look. But diagnosis is not prevention. The question is what control structure actually addresses all three legs simultaneously for non-human actors.

The answer is not a better score. Scores are probabilistic. They tell you something is likely or unlikely. In a world where agents can execute thousands of transactions per second, a 2% false negative rate is not a rounding error. It is a fraud operation running at scale inside your acceptable loss tolerance.

What merchants and platforms actually need is a verification record: a cryptographically signed artifact that attests, at the time of the transaction, that a known agent was operating within a defined scope, from a verified environment, under the authority of an identified principal. Not a probability. A record.

That record addresses all three legs of the fraud triangle directly. The identity leg is addressed by the principal attestation and the agent's authorization scope. The device leg is addressed by the runtime environment signals embedded in the record. The cashout leg is addressed by the scope constraints that define what the agent was and was not authorized to do.

If the transaction later turns out to be fraudulent, the record tells you exactly where the chain of authorization broke. If the record was forged, the cryptographic signature fails verification. If the agent exceeded its scope, the record shows it. If the runtime environment was compromised, the signals in the record reflect that.

This is not a new idea. It is the same logic that 3-D Secure applied to card payments two decades ago. The card network needed a way to shift liability from the merchant to the issuer when the cardholder's identity was verified at the time of the transaction. The verification record does the same thing for agent commerce, on rails that were not designed with any of this in mind.

What Comes Next

The fraud triangle is not going away. Every scheme that gets built on agentic rails will still require an identity, a device, and a cashout mechanism. What changes is the cost and speed of assembling those components, and the inadequacy of controls that were never designed to evaluate non-human actors.

The builders who are thinking about this now, before agent commerce reaches the scale where the losses become undeniable, are the ones who will have the infrastructure in place when it matters. The builders who wait will be retrofitting controls onto a payment stack that was never designed to support them.

The fraud triangle has not changed. The entity committing the fraud has.

If you are working on agent payment rails and want to talk through how the fraud triangle maps to your specific stack, write to contact@flint.network.

Get in touch

If you are building on agentic payment rails and want to talk through how FLINT fits your stack, reach out directly.

contact@flint.network